Why Funding a Franchise Start-Up Is Often Easier Than Funding an Independent Business Acquisition

A Shortsighted Assumption

One of the most common assumptions among aspiring business owners is that buying an existing business is less risky and therefore easier to finance than starting a new franchise location.

While that can sometimes be true from an operational standpoint, the reality is often very different when it comes to obtaining financing.

In today's market, many buyers are discovering that funding a franchise start-up with a mature, established brand can be significantly easier than funding the acquisition of an independently owned business.

The SBA Loves Predictability

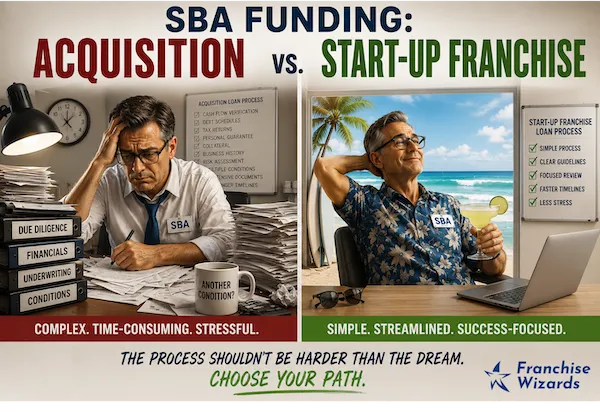

Most small business acquisitions rely heavily on SBA financing. When a lender evaluates a loan request, they are not only assessing the buyer. They are also evaluating the business itself.

A mature franchise system offers several advantages:

Established operating procedures

Proven customer acquisition methods

Recognized brand awareness

Historical performance data from multiple locations

Franchisor training and ongoing support

Benchmarking against hundreds of existing franchisees

Because of this, many franchise loans fit neatly into lender programs designed specifically for franchise financing. Certain lenders can process these opportunities through streamlined underwriting channels, often resulting in a faster and more predictable approval process.

While every transaction is different, lenders frequently view a mature franchise start-up as a lower-risk proposition than an independent business acquisition because there is an entire support system standing behind the new owner.

Lenders Pay Attention to Default Rates

Banks are not in the business of creating entrepreneurs. They are in the business of managing risk.

One of the reasons many lenders are comfortable financing mature franchise brands is the historical performance data available across hundreds, and sometimes thousands, of locations.

Unlike an independent start-up, where the lender has limited visibility into future performance, established franchise systems often have years of operational history, validated business models, and measurable performance benchmarks.

This is a critical distinction.

The lender is not evaluating a brand-new, unproven concept. They are evaluating the replication of a business model that has already been tested across multiple markets, economic cycles, and ownership groups.

As a result, many mature franchise systems have historically demonstrated relatively low loan default rates compared to what many people assume when they hear the word "start-up."

From the bank's perspective, financing a first-time owner opening a location within a mature franchise system can sometimes be more predictable than financing the acquisition of an independent business whose success may depend heavily on the departing owner, key employees, or unique local circumstances.

That predictability is one of the reasons many franchise loans receive favorable consideration from SBA lenders and why some franchise transactions can move through the approval process more efficiently than independent acquisitions.

The Acquisition Myth: Are You Really Buying Less Risk?

Business acquisitions are often perceived as a shortcut to success.

After all, the business already has customers, employees, revenue, and operating history. Many buyers automatically assume that this translates into lower risk.

The reality is more nuanced.

The risks are not necessarily lower. They are simply different.

Unless you are acquiring a business under very special circumstances, such as an intra-family transaction, partner buyout, or another highly favorable situation, you are typically paying a premium for someone else's past success.

Let that sink in.

The seller spent years building the customer base, developing systems, hiring employees, solving problems, and creating value. When you buy that business, you are paying for those years of effort through a multiple of earnings.

In many cases, the acquisition buyer is purchasing an asset after much of the value creation has already occurred.

By contrast, when you invest in a start-up, you are sitting on the other side of the table.

You are not paying a premium for past success.

You are creating future value.

If the business grows successfully, develops a strong customer base, builds recurring revenue, and establishes a market presence, one day you may be the seller receiving a premium valuation from the next buyer.

This does not make start-ups safer than acquisitions. It simply highlights that the risk profile is different from what many buyers assume.

The Hidden Challenge of Independent Business Acquisitions

An independent resale may have years of operating history, but lenders must evaluate much more than the buyer's qualifications.

Questions often include:

Are the financial statements accurate?

Do tax returns support the reported earnings?

Is revenue concentrated among a few customers?

Will key employees remain after the sale?

Is the owner the primary reason for the business's success?

Are there any hidden liabilities?

Has the business been underinvested?

Are the reported earnings sustainable after the transition?

As a result, underwriting tends to be more complex and time-consuming.

The lender is essentially financing a unique business with no franchise infrastructure, no standardized operating system, and no support organization standing behind the new owner.

The SBA Pre-Approval Letter Is Not a Golden Ticket

Many buyers gain confidence after obtaining an SBA pre-approval letter.

Unfortunately, some misunderstand what that document actually means.

An SBA pre-approval does not mean the bank has approved a future acquisition.

It simply means that based on your personal financial profile, liquidity, creditworthiness, and experience, you may qualify to borrow up to a certain amount under ideal circumstances.

The target business must still qualify on its own merits.

The lender will still analyze:

Historical financial performance

Tax returns

Debt service coverage ratios

Customer concentration

Industry-specific risks

Management continuity

Quality of bookkeeping and financial reporting

Overall transaction structure

In other words, the business itself must successfully underwrite.

A buyer may be pre-qualified to purchase a $1 million business, but if the target company does not satisfy the lender's underwriting standards, the deal may never receive final approval.

The pre-approval letter simply tells you your potential buying power under perfect conditions. It is not a commitment to finance every acquisition opportunity you pursue.

The Competition Problem Nobody Talks About

Even when an acquisition qualifies for SBA financing, another challenge has emerged in recent years.

You are no longer competing only against other individual buyers.

You are increasingly competing against:

Private equity firms

Family offices

Search funds

Independent investment groups

Strategic corporate buyers

Many of these buyers are sitting on substantial cash reserves and do not require SBA financing.

While an SBA-funded acquisition may require:

Letter of intent

Due diligence

Lender underwriting

SBA approval

Closing process

The timeline can easily stretch 45 to 60 days, and sometimes longer.

Meanwhile, a well-capitalized investment group can often close much faster.

From a seller's perspective, certainty and speed matter.

A seller may prefer a slightly lower cash offer with fewer contingencies over a higher offer that depends on financing approval and a lengthy underwriting process.

The reality is that if your acquisition strategy depends on SBA financing, you are often 45 to 60 days slower than some of your competition before the race even begins.

Why Good Businesses Rarely Stay Available

The highest-quality resale opportunities tend to attract immediate attention and often change hands within the seller's professional network, never even reaching the public market.

Businesses with:

Strong cash flow

Recurring revenue

Stable management teams

Diversified customer bases

Clear growth potential

are precisely the types of businesses that attract sophisticated investors.

The biggest challenge is often not losing a deal during underwriting. It is getting a seat at the table in the first place.

Many of the most attractive businesses are acquired by industry buyers, family offices, search funds, private equity groups, and private investors before they ever appear on public marketplaces.

As a result, individual buyers often find themselves competing for a limited inventory of opportunities, while the most desirable businesses are quietly changing hands behind the scenes.

Why Many Investors Are Turning Toward Franchise Start-Ups

A franchise start-up avoids many of these challenges.

Instead of competing against private equity firms and family offices for a limited inventory of attractive businesses, investors can secure:

Protected territory rights

New market development opportunities

Proven operating systems

Established brand recognition

Franchisor training and support

More straightforward financing options

Most importantly, there is no seller deciding between competing offers while your financing is being processed.

Once the franchise agreement and territory are secured, the investor can focus on building the business rather than winning a bidding war.

And if the business is built successfully, the owner may ultimately become the person selling a valuable asset at a premium multiple years down the road.

The Bottom Line

Business acquisitions can be excellent opportunities, and there are situations where acquiring an existing company makes perfect sense.

However, buyers should understand what they are actually purchasing.

In most cases, they are paying a premium for value that someone else has already created, while assuming a different set of risks than many realize.

At the same time, obtaining an SBA pre-approval letter is only the beginning of the financing process, not the finish line. The target business must still pass underwriting, and the acquisition must compete against buyers who often have the ability to move much faster.

Ironically, many buyers view a franchise start-up as the riskier option because it starts at zero revenue. Yet from the lender's perspective, a mature franchise system with strong historical performance, established operating procedures, franchisor support, and relatively low default rates may represent a more predictable risk than acquiring an independent business at a premium valuation.

The question is not whether acquisitions are good or bad.

The question is whether you fully understand the trade-offs before choosing your path to business ownership.

The Biggest Risk Might Be Doing Nothing

One final thought.

What is the cost of waiting?

Over the years, I have spoken with countless prospective business owners who were convinced that the perfect acquisition was just around the corner.

Some have been searching for one year.

Some for three years.

A surprising number have been searching for seven years or more.

Think about that.

During those same seven years, they could have:

Selected a proven franchise model

Opened their doors

Endured the start-up phase

Built a customer base

Stabilized operations

Expanded into additional territories

Created meaningful enterprise value

In some cases, they could already be preparing for an exit.

Instead, many remain on the sidelines waiting for the perfect deal, the perfect valuation, the perfect financing structure, or the perfect market conditions.

The reality is that there is a cost to inaction.

While buyers focus on the risks of starting a business, they often overlook the risks of waiting indefinitely.

Time is the one asset that cannot be replenished.

The question is not whether a franchise start-up or business acquisition is the better path.

The question is whether your current strategy is moving you closer to your goals or simply keeping you in perpetual search mode.

At some point, the opportunity cost of waiting becomes greater than the risk of taking action.

Let's Have an Honest Conversation

If you have been searching for the right business acquisition for months, or even years, I would like to invite you to a candid conversation.

Not a sales pitch.

Not a presentation.

Just an honest discussion about whether a mature franchise start-up deserves consideration as a Plan B, or perhaps as an alternative path to business ownership altogether.

Many of the prospective investors in our database have spent years chasing the perfect acquisition. During that time, they could have selected a proven business model, completed the start-up phase, built a customer base, stabilized operations, expanded, and begun creating meaningful enterprise value.

Franchising is not the right investment vehicle for everyone.

Our job is to help you determine whether it should be part of the conversation.

If you are open to exploring that possibility, schedule a complimentary Strategy Session.

You may walk away confirming that an acquisition remains your best path.

Or you may discover that the opportunity you have been searching for is one that can be built rather than bought.

Either outcome is valuable.

Schedule a complimentary Strategy Session and let’s determine whether franchising is the right path for you.

Our consultation and franchise matchmaking services are complimentary to prospective investors.